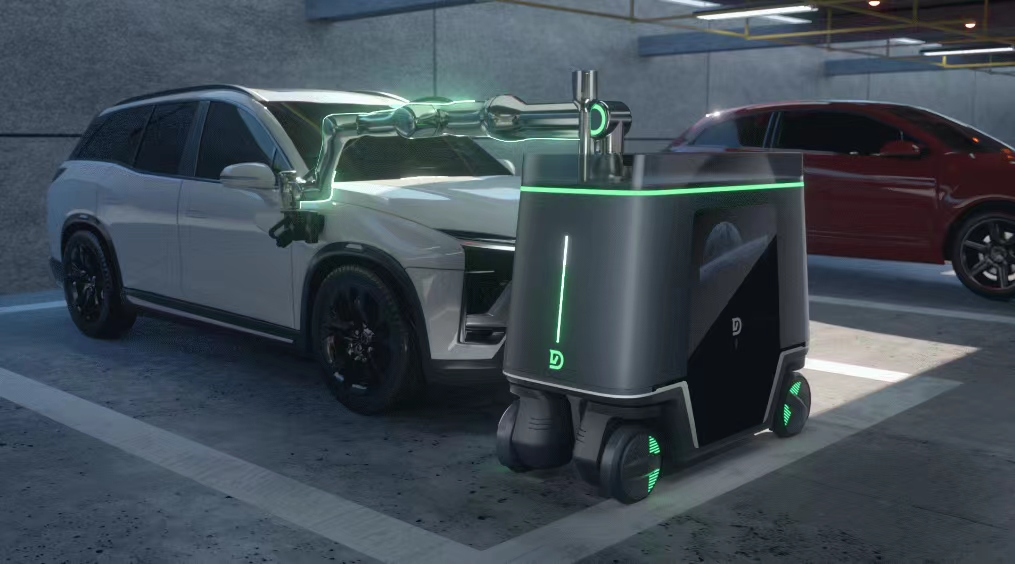

Tier 1 Smart Driving, another opportunity is about to take off? As electric vehicles continue to struggle to find a fixed charging station, the idea of large-scale “mobile charging stations” is becoming more feasible. Many car manufacturers, power battery companies, and even Tier 1 companies are exploring this possibility. Furthermore, with the development of artificial intelligence, the robotics industry, especially those with embodied intelligence, is entering a market worth billions of dollars. Tier 1 Smart Driving’s “cross-border” mobile charging robot According to the latest data released by the China Association of Automobile Manufacturers, in 2023, the production and sales of new energy vehicles reached 9.587 million and 9.495 million respectively, an increase of 35.8% and 37.9% year-on-year, with a market share of 31.6%, an increase of 5.9 percentage points from the previous year. Despite the rapid development of new energy vehicles, range anxiety and charging anxiety remain industry pain points. According to Cui Dongshu, Secretary General of the China Passenger Car Association, the ratio of pure electric passenger cars to public charging piles is 3:1. However, due to imperfect charging technology and infrastructure, problems such as difficulty in charging, difficulty in finding piles, queues at service areas during peak hours, low installation rates of old charging piles in old communities, occupied charging spaces, insufficient utilization of fixed charging piles, and high failure rates continue to plague the industry. Recently, Tang Rui, founder and CEO of Zongmu Technology and Cancong Robotics, stated, “The charging business for new energy vehicles is actually very bad, with high investment but very low asset efficiency. The average utilization rate of each charging pile in the industry is less than 6%.” In addition to car manufacturers and battery-related companies, even autonomous driving companies are starting to think about this issue. Recently, Zongmu Technology announced the launch of its new subsidiary Cancong Robotics and its new product, the FlashBot. This product is not only an energy robot, but also serves as a “mobile charging station” for new energy vehicles. It is equipped with L4 level intelligent driving capabilities and a 104KWh capacity, providing intelligent charging services for new energy vehicles in scenarios such as parks and parking lots.

As a company dedicated to promoting the large-scale production of L4 autonomous driving, why expand business to mobile charging robot field? Currently, although the relevant policies for promoting L3 autonomous driving have been introduced, it is still in the access and trial stage, and problems such as incomplete map surveying of underground parking lots, immature L4 autonomous driving technology, and division of responsibilities are difficult to solve in the short term. The commercial progress of advanced autonomous driving for passenger cars has been difficult, leading any autonomous driving company to seek a “second business” to generate profits. The business model of car power bank and mobile energy storage terminal is a feasible “cross-border” track. Zongmu Technology has always focused on the early development of AVP technology for autonomous valet parking in low-speed scenarios. However, Tang Rui stated that before the large-scale implementation of autonomous valet parking, FlashBot will be the product that will achieve the commercial application of autonomous valet parking in closed parks. According to its analysis, with the rapid growth of new energy vehicles and clean energy such as wind and photovoltaic power, the past centralized energy network will quickly transition to a distributed energy network. Matching the random distributed energy supply and demand through fixed infrastructure investment is a process of inefficient resource allocation and inefficient asset investment. Tang Rui mentioned that, by combining the mobility of autonomous driving with energy storage batteries, it is possible to match the supply and demand of distributed energy in a larger space and time, providing more convenient energy exchange and achieving efficient asset utilization. Industry insiders say that mobile charging robots have huge potential in special scenarios such as highways during holidays, underground parking lots that do not allow charging piles or have large-scale assembly periods, ports during assembly periods, and home or tourist attractions. It is understood that Flash Power uses peak shaving and valley filling electricity price arbitrage storage business as the foundation, and uses car charging business as the value-added profit model. According to the trial operation data that started at the end of November last year, each Flash Power can achieve a net income of 200 yuan (30$) per day on average. Two Flash Power units purchased 272 kWh of electricity from the park microgrid daily in December, of which 185 kWh were sold back to the park microgrid, with about 80 kWh sold at peak electricity prices and the remaining 90 kWh used to provide charging services to park vehicles. Based on this, the return period is about 3-5 years.

“Mobile Charging Robot” enters the “fast lane” of development It is worth noting that the concept of “mobile charging treasure” or mobile charging robot is not a new thing. It has been the focus of the industry as early as three or four years ago, and has begun to enter the “fast lane” of development in the past two years. Including car companies such as Tesla, Volkswagen, and FAW Hongqi, battery companies such as Farasis Power and Guoxuan High-tech, charging and energy internet related companies such as Nenglian Zhidian and Zhineng Dianqi, and technology companies such as Heima Yuanli and Shitu Technology have all launched mobile charging robots, some of which have achieved automatic plug-and-pull charging guns. Especially in 2023, the release of related products has become more and more intensive. For example, in March, Nenglian Zhidian launched a self-developed charging robot, which was also showcased at CES 2024. According to its plan, the product will be first deployed in the high-speed service areas of Hubei and Hainan, and gradually promoted nationwide. During the Shanghai Auto Show, not only Lotus showcased its independently developed mass-produced “flash charging robot”, but Heima Yuanli also launched its first MPS product – G60 Xiahei, greatly increasing the utilization and rotation rate of charging facilities.

In the same year, Tesla showcased a mobile supercharging station in Las Vegas with a maximum charging power of 750 kilowatts. In addition, a mobile charging station developed by Guoxuan High-tech officially went “on duty” in Hefei, with 400 of these robots already in use and plans to deploy no fewer than 1000 more in the future. For companies like Zongmu Technology and Heima Yuanli, the ultimate goal of deploying mobile charging robots and iterating on their technology is to build a highly flexible mobile energy network, enabling energy trading in a wide range of time and space. However, it must be pointed out that automatic charging is a relatively new form of energy replenishment, and the commercial model for the industry application of mobile charging robots is still in the exploratory stage, thus facing various challenges. Nenglian Zhidian has previously pointed out that there are still technical issues such as precise identification and positioning of charging ports in complex environments, as well as the lack of clear standards and pathways for the operation, asset management, and commercial services of mobile charging robots, all of which require further exploration and development. Overall, the new track of mobile intelligent charging equipment, which combines concepts such as autonomous driving, energy storage, charging, and robots, is expected to become a new opportunity. In the future, with the advancement of artificial intelligence technology, it will inevitably attract more capital and “cross-border” players to join. Combining with the research report of the autonomous driving market research institution Navigant Research, the commercialization of mobile charging solutions currently accounts for 0.5% of the entire electric vehicle charging equipment market, and is expected to reach 2% by 2030, with the market size expected to grow from $16 billion in 2020 to $60 billion in 2030. Is the industrial chain escalating, and the industrialization of humanoid robots imminent? When it comes to the development of robots, it is impossible not to mention the direct surge of hot air in the field of robots brought about by the 2023 AI large model. The rapid advancement of mobile charging robots today is also inseparable from the transformation of artificial intelligence and autonomous driving technology. Looking at the entire robot industry, from specialized to general-purpose, the industry has seen an upgrade in application scenarios. It is worth noting that the subfield considered to be at the top of the robot industry pyramid is humanoid robots. The latter, using embodied intelligence and large models, can handle a variety of application scenarios and is seen by the industry as the best carrier of AGI.

According to Tesla CEO Musk, humanoid robots have more potential than electric cars. Assuming a 2:1 ratio of robots to humans, the demand for humanoid robots is expected to reach 10-20 billion units, far exceeding that of cars. The trend of “embodied intelligence” in the robotics industry is undeniable. In terms of policy, at least 8 policies have been introduced in the past three years to support the development of the robotics industry. In particular, the “Guiding Opinions on Innovative Development of Humanoid Robots” issued by the Ministry of Industry and Information Technology in November 2023 clearly states that humanoid robots, integrating advanced technologies from various fields, are expected to become another groundbreaking product after new energy vehicles. Looking at the progress of the industry chain, with the intensive launch of related products and gradual entry into the manufacturing industry, it is widely believed that 2024 will be a key period for humanoid robots to move from the prototype stage to mass production and application. The latest “Humanoid Robot Industry Report” released by the GAC Research Institute also points out that the application of humanoid robots is being driven by the continuous upgrade of AI large models, and mass production is expected within the next two years. The initial commercialization will mainly focus on industrial and exhibition fields, bringing broader prospects for the application of humanoid robots.

In early January of this year, Tesla’s two automotive suppliers, Top Group and Sanhua Intelligent Control, successively announced investment plans for robot production bases with a total scale of over 10 billion yuan, which was considered by the industry to be a landmark event marking the commercialization of humanoid robots. Recently, BMW’s joining the humanoid robot army has once again ignited the track, with its pilot application at a factory in Spartanburg, South Carolina. In addition to BMW, car companies such as Tesla, Honda, Hyundai, Xiaopeng Motors, and BYD have also entered the field of humanoid robots. Among them, as a representative enterprise that has heated up the humanoid robot track, Tesla’s release of the second-generation Optimus robot in late 2023, priced at tens of thousands of dollars, further increases the possibility of large-scale production of humanoid robots. Domestically, Xiaopeng Motors is also one of the earlier car companies to start the layout of “car + robot”. Since 2016, it has been developing quadruped robots and showcased the bipedal humanoid robot PX5 in October last year. In addition, many technology companies have already made strategic layouts, such as Engineered Arts in the UK, Agility Robotics, Apptronik, and Figure in the United States, and the Norwegian company 1X’s humanoid robot has achieved a certain degree of commercialization. Domestic technology companies such as UBTECH, DT Robot, Ubtech, ZhiMi Technology, Huawei, Xiaomi, iFlytek, ByteDance, and Zhiyuan Robot have all launched related products. For example, UBTECH, as the first domestic “humanoid robot stock,” has already landed its first batch of humanoid robots “Walker X” in the new future city of Saudi Arabia; and Xiaomi entered the humanoid robot track in 2022, showcasing the first full-size humanoid bionic robot CyberOne, equipped with self-developed visual spatial system and audio algorithms in the same year. At the CES 2024 summit, companies including Ubtech, Kepler, Boston Dynamics, and UBTECH all “showed off their muscles,” with Kepler’s humanoid robot product pioneer K1 and Ubtech’s H1 directly competing with Tesla’s Optimus.

UBTECH co-founder, Chief Technology Officer and Executive Director Xiong Youjun believes that after half a century of development, humanoid robots have reached the stage of industrialization, and their commercial application trends and landing scenarios have become more certain. “Humanoid robots are the best carrier of embodied intelligence. They will transform the interaction mode of human-machine cooperation from passive interaction to active interaction and natural language interaction. Therefore, they will be the next generation of human-machine interaction center, and even become a truly ‘intelligent terminal’, with huge long-term value.” However, Professor Xi Ning, Chief Scientist of the Shanghai Humanoid Robot Innovation Incubator and Director of the Institute of Emerging Technology at the University of Hong Kong, also stated that the mass production of humanoid robots is not a simple matter of going from 0 to 1, but a gradual process of evolution. “Humanoid robot systems contain many complex components, and key components and technologies need to be achieved and mass-produced before the overall system can be mass-produced.” The Gaishi Automotive Research Institute also analyzed that, referring to the classification of intelligent driving systems, humanoid robots need to reach a level of L3 or above to achieve autonomous control. In this process, the commercialization of humanoid robots will face the dual challenges of intelligent autonomous movement and cost reduction. Of course, from a long-term perspective, Tesla’s previously announced long-term product sales price not exceeding $20,000 is expected to lead the pace of industrial commercialization. The Gaishi Automotive Research Institute predicts that by 2030, the average selling price of humanoid robots will decrease from 459,000 yuan (64690$) to 162,000 yuan (22830$), a decrease of 65%; sales will reach 2.16 million units, with a total market size of 350.6 billion yuan.

In conclusion Whether it’s the iteration of AI large model technology, the mass production conditions of the entire industry chain, or the consideration of cost and policy regulations, the process of robots truly “growing up” is bound to be long and full of challenges, but this does not prevent capital and enterprises from entering the game and embracing the future billion-dollar blue ocean market. With the advent of the general AI “singularity” and the continuous reduction of robot hardware costs, the large-scale industrialization of humanoid robots may accelerate.